It is also the title of a David Bowie song from way back in the early 1970’s, way before the internet, but not door to door van deliveries. My ‘Old Mum’ used to give her greengrocer a written list and he delivered it to the front door a day later. And she was doing that in the sixties. No internet, no iffy broadband, no crashing web sites, no ‘out of battery‘ phones. Pen, paper, man in greengrocer and a green van ( colour that is, not in the slightest bit eco-friendly) . Simples as a wise Meerkat once said.

That Greengrocer eventually closed because of the rise of the supermarket. What do you make of that because my mother then had to drive to get her greengroceries. Now, it was not down to my mother that all independents closed, but there is some irony in that some consumers lost an element of convenience in the name of convenient shopping.

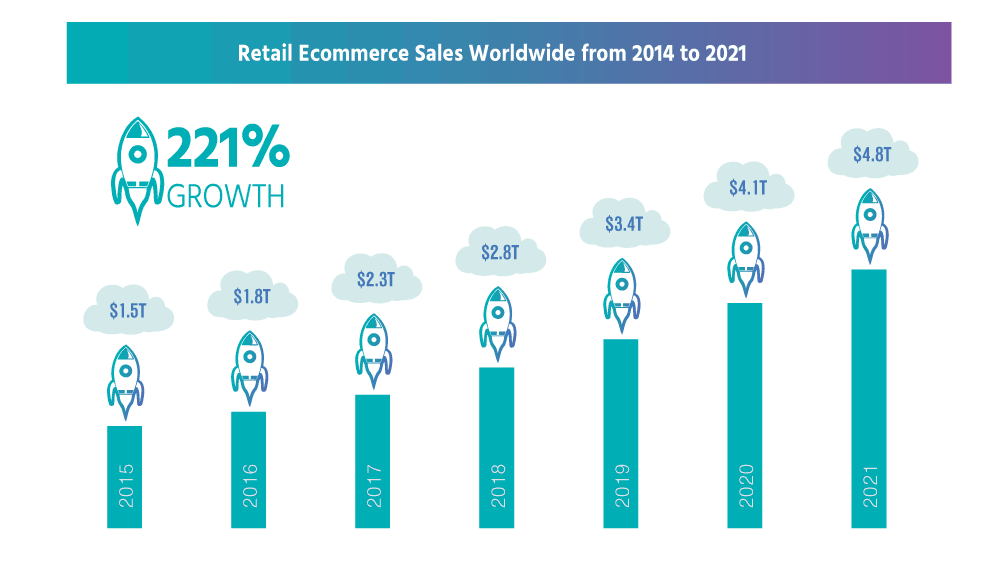

Race forward sixty years and we are back to delivering our purchases via a method somewhat more complex than pen and paper. Before the shout goes out about the Internet killing the retailer , unfair competition blah, blah, blah., lets just take a gander (Look for non native English speakers of whom I know there are a few , or at least one or two)over the last 18 months . With the various lockdowns throughout Covid, the retail environment would have been even more dire. Dare one say the emotional health of the nation would have been somewhat worse the wear, in that costumers were , when finances allowed, able to indulge in a huge variety of product, whether books ,puzzles, hobbies, household products, clothing , all product that was not essential but enabled a slightly better environment when you were confined to your own four walls.

So if we can make the case that all online operations are not all bad then I think it is only fair to look at the case as to why they should not get quite the bad press most of the media seems to give them .

There are broadly 3 types of B2C operators

Those who sell on the market places eg Amazon, eBay & Etsy etc

Those that operate their own Web shops

The Third being those who operate on both

Let’s examine the the second ie those who trade via their own web shops.

Before doing that it is important to make thing clear about online operators , for the most part they do not operate on the High Street therefore their rent and rates will tend to be lower than a Bricks and mortar equivalent per square metre. There ends in my view their main economic cost benefit .

Basic Higher Costs for Web shop operators Vs Bricks and Mortar

1.Unit size tends to be much larger than equivalent bricks and mortar

2.Stock holding is likely to be much higher

3.Technology both hard and soft high cost of entry due to much greater demands on the systems

4.Greater number of SKUs-Independent brick and mortar (in Party) maybe 6000+ ,web shop more like 30,000+

5.Can take up to 30 minutes to load one new product onto a web shop (that is similar for the market places, if not more so)

6.Very high cost of marketing or web awareness. It would be no exaggeration to say this can be in 6 figures

7. High cost to maintain awareness

8. Cost to deliver (no cost to Bricks and mortar). Current major issue is a problem concerning shortages of drivers

9. High cost to maintaining customer loyalty (Since there is no face-to-face interaction like in a retail store, the development of trust and loyalty takes more time and effort in eCommerce)

10. Cost of returns (Over 60% of online shoppers look at a shop’s return policy before making a purchase.)

11. Cost to pick and pack

12. Increasing IT requirements such as data analysts

These are just some of the cost issues. Other barriers facing B2C e commerce platforms are (all involve cost at some point)

Online identity verification

Overall cyber security

Shopping Cart Abandonment (apparently this can amount to anything between 60-80% )

Many of these issues can be offset by using the market places such as Amazon & eBay. Yet these have their own pitfalls in terms of there is, of course a cost, pricing is very aggressive, you can be competing against a far bigger supply chain, and you are reliant upon the whims the platform you are using and subject to their rules.

Here’s a fascinating little fact

It takes about 50 milliseconds (that’s 0.05 seconds) for users to form an opinion about your website that determines whether they like your site or not, whether they’ll stay or leave.

sweor.com

and another …….

47% of Users expect a maximum of 2 seconds loading time for an average website

sweor.com

yet another ….

Users spend an average of 5.59 seconds looking at a website’s written content

sweor.com

Take the sum of these 3 stats and you are not looking 8 seconds in total. It takes that long to walk into a shop before you have begun to get an impression of what is on offer. That said there are some retailers where I have made a very precise decision not to enter in a fraction of that time , which will say loads about those particular shops.

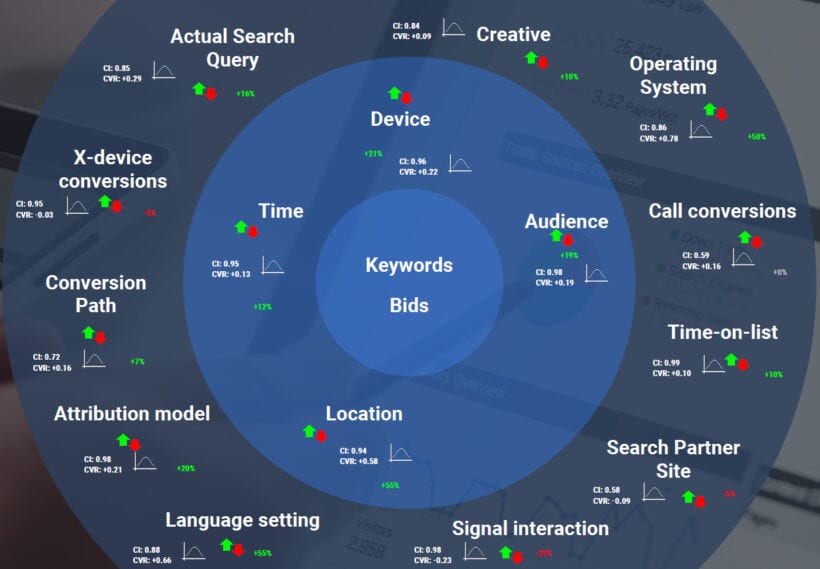

The following diagram may also illustrate how being an online seller is not that straight forward. Show me a bricks and mortar retailer that is faced with any of these dilemmas.

Governments have talked much about taxing the ‘ so called‘ advantages of the online operators . There maybe an argument for the likes of Amazon, but for the rest it is taking a sledge hammer to crack a nut. There has never been an argument for additional taxation for the supermarkets . Tesco & Sainsburys alone take over 42% of the market. Who had it before they existed (as supermarkets) ? The independent retailer . It is how retail evolves. The market place has to adapt as it always has. Nobody said it was going to be easy.

No Retailing is easy. It never has been, and it wont get any easier. It has to evolve to survive. There will always be the ‘naysayers’. Online is here to stay and so are good bricks and mortar retailers , we started with Bowie so I’ll finish with Ike & Tina Turner

Working together we can make a change

Working together we can help better things

Ike & Tina Turner 1970

Bit of a shame Ike didn’t think more about some of the words he sung , but that does not detract from the essence .