I am a clumsy bastard . I know it. Very recently, I knocked over a prized piece of pottery from a Pottery in County Cork. It was much loved by Julia, and whilst she did not banish me from the house, there was a very small tear in the corner of her eye.

Surreptitiously, I did a little research and found the Pottery and its website. As there was a label still attached to the underside of the piece. It had the item number and the price we paid in 2015. Eleven years later, the price was exactly the same.

There is a Malaysian restaurant in North London that we have visited every so often for over twenty-five years. The Satay is exquisite, and the Beef Rendang is the best I have had outside of Malaysia. I may not go on to say the prices have not changed, but they have not changed much. The quality of the food has not changed at all.

Even in 1972, the price of a colour TV was £225 (£3,158.93 in 2022 costs), a slight reduction from the late 60s of £304 (£5,610.01). However, with the introduction of colour TV, the price of black and white displays remained somewhat expensive at £186.40 (£4390) in 1960.

In the 1980s, second-hand sets and ex-rental models were more affordable for individuals. It is reported that buying a TV set used for rental purposes would cost £12 (£40.60). In comparison, a brand new TV in the 80s would cost £109 (£372) for a black and white set, or for a more advanced colour TV you would expect to pay £254 (£868). The Cost Of TVs Over The Years

Today John Lewis ( not the average retail discount operation ) has a 40″ smart tv on line for £143.

In 1988 the price of a Kilo of bananas was approximately £1.06; in June 2019 it was £0.94 (Which Report)

In 1980 a Casio scientific calculator cost about £13 (Boots) , you can now buy one on Amazon for less than a tenner.

A Warburtons standard white loaf is now (in Tesco’s) (May 2026) £0.05p cheaper than it was in 2010 (£1.40 vs £1.45)

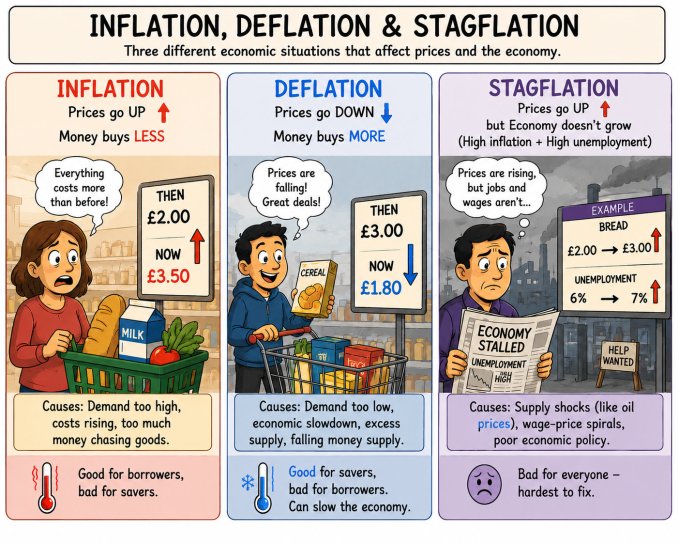

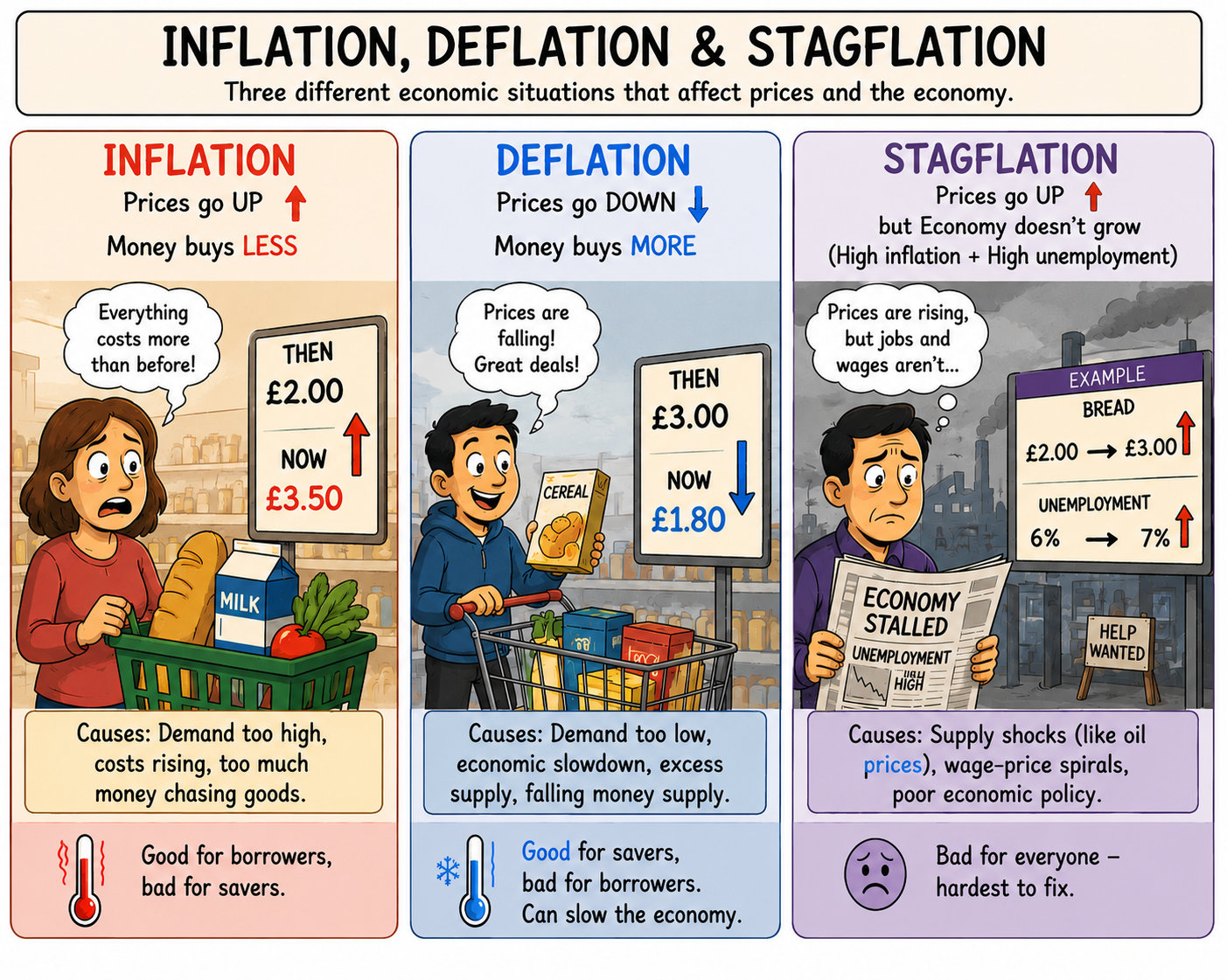

I am not quite stupid enough to suggest that there is no cost-of-living crisis. Quite clearly, there is, although where the cost impact lies can be challenged. Food has clearly gone up, yet the average household spend has dropped from nearly 30% of total income in the early sixties to a figure approximating 11% in 2025 (this was nearer 8% in 2020). There are a lot more calls and pressures on the family budget that did not exist sixty years ago. Tv’s maybe a lot cheaper, but dramatic change in technology has led to additional costs, some of which are choice (streaming) others not so much (internet/broadband connections). All, of which relate to the way we earn and spend our money. It is not a straight line connection between now and sixty years ago.

Greedflation was publicly criticised by US politicians and European central bankers, who pointed to data that suggested corporate pricing behaviour was making the world’s inflationary problem much worse. Philip Lane, chief economist at the European Central Bank (ECB), cited “extraordinary unit profits” as a factor driving near double-digit inflation in the bloc in 2023. A study from the International Monetary Fund said rising profits were responsible for 45 per cent of the eurozone’s inflation headache from 2022-23.

Four years on, the world economy is back in the grip of an energy supply shock that threatens to stoke inflation far above central bank targets. One question worrying policymakers is whether greedflation is coming back. -The Times May 30th 2026

I digress , just a bit .

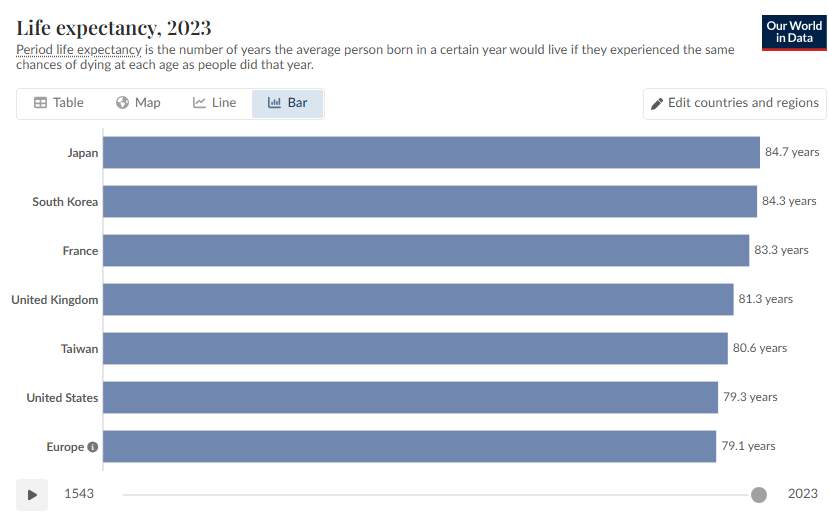

There are few examples of prolonged stagnation and deflation. But, perhaps, the biggest is that of Japan. In the 1990’s the Japanese economy experienced what is known as the ‘Lost Decade’. Reasons are manyfold and open to debate but broadly speaking, it was due to an asset bubble and weak monetary policy. However, despite various attempts, little has changed over the next two decades where annual growth has been grinding along the bottom at less than 1%. Government policy has aimed for inflation rates of 2%, but for many years barely exceeded 0%. Naturally, this has huge impacts upon its general economy (at worst it had a debt ratio of over well over 200%-2026 204% -Statista – and we get excited when it hits 100%). It has gone from 1990 being the World’s second largest economy to now being the Worlds fourth largest.

But how tough is life in Japan? Major Japanese companies such as Toyota, SoftBank, Mitsubishi, Sony and The Fast Retailing Group (Uniglo), to name just a few, would suggest they are not quite in the Third World yet.

Hannah Ritchie (2026) – “Population and Demography” Published online at OurWorldinData.org. Retrieved from: ‘https://ourworldindata.org/profile/population-demography/japan’ [Online Resource]

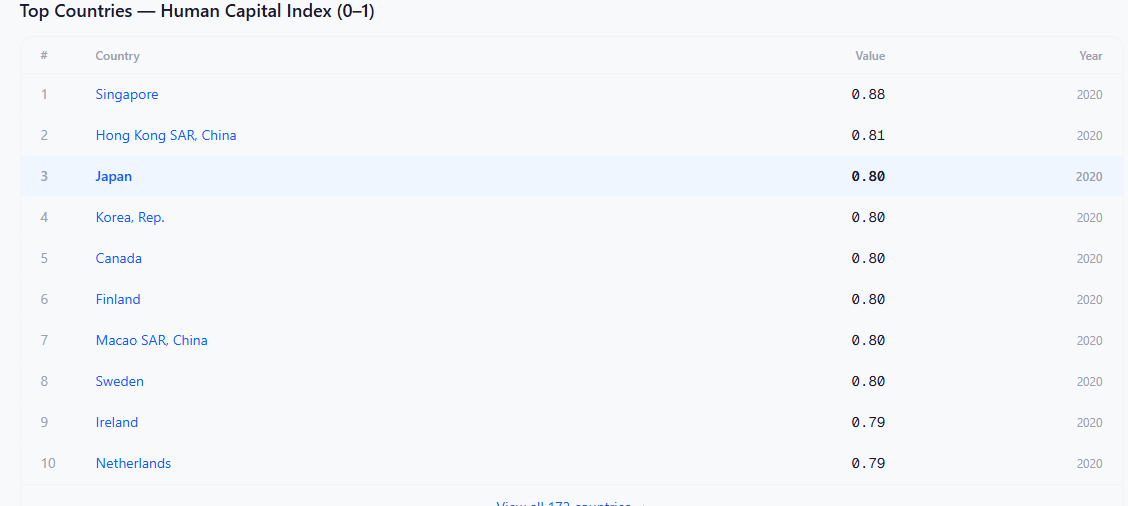

- The Human Capital Index (HCI) is an annual metric developed by the World Bank to assess how effectively countries are mobilizing their human capital, which includes the knowledge, skills, and health of their citizens

Japan is the world’s largest net creditor nation, holding trillions of dollars in foreign assets. Sunnyside Financial Group.

So what is all the ‘Japan’ bit about? Personally, I am fascinated by Japan, its culture, food, history, design and have been fortunate to have visited the country. But all that is a personal view and totally irrelevant. Japan is the only ‘first world‘ democratic country to have experienced long-term (over three decades ) virtual stagnation. Yes, it has had its financial problems and still has (as have many advanced democratic economies), but remains a reasonably well balanced society .

It is difficult to say how many Japanese are technically “poor” in Japan, but it is safe to say that we do not easily find rows of houses and families living in terrible conditions or people starving. Japan hides poverty so well that we can hardly imagine that there are poor Japanese people.

Kevin Henrique · Jan 16, 2026

Clealry, there is poverty, yet on most measures of poverty it is not as bad as it is in the States.

This is taken from a site called Statistics of the World, in turn taking its data from the World Bank and the IMF. However, I have to say, having looked at various data sets, the way these indices are measured seemed slightly bonkers. According to this same set of data Iraq has lower poverty rates than Japan and the US.

My thought process stems from a late-night discussion with an Irish friend, while imbibing some glasses of Guinesses, over my belief that the pursuit of growth has to stop sometime, as our planet is a closed system of finite resources. My friend strongly disagreed. There are, of course, holes in my theory as there in the Earth’s atmosphere that protects this system. But my overarching point is that do we have to consider capitalism and social economics in a less traditional way? And come up with a completely different way of looking at things.

One the tag lines used by Guinness is:

Out of the darkness comes light.

The light has yet to come.

Or as the Japanese say:

“Ashita wa ashita no kaze ga fuku”

Translation: “The winds of tomorrow will blow tomorrow”

Meaning: Do not be worried about your bad situation because things change over time