Being the season of goodwill and all that. Everybody is reading about :

127 ways of roasting a turkey/goose/chicken

Why do the British put cream/custard/ice cream on meat pies (mince pies-for all Non Brits) ?

How to feed a family of four at Christmas for £1.78

Why a Local Vicar is telling small children that Father Christmas does not exist

I felt the need to write something completely inappropriate and what could be more inappropriate than National Insurance Contributions.

I try very hard not to say anything about politics, there are bucket loads of people who can do that for better or for worse . I am politically disenfranchised . I think those on the left, on the right and the centre have lost the plot . And not just in the UK .

Therefore, my question here is not aimed, in this case against the Labour party or their last budget , about which I have many other more pressing questions, but the effect it will have or not have on UK Businesses.

UK Business Plc is jumping up and down, screaming from the roof tops that it is sheer madness and will make prices will go through the roof or the entire economy will collapse over night. Whilst I dont’t think it will induce growth , and I think there are better ways to fill the black holes, if you drill down, I need to be illuminated as to why it will have such a detrimental impact on costs and then prices in the way that is being suggested .

A rise of 1.2% on a rate of 13.8% significant. The calculation I have found is that this will make a increase for an organisation employing somebody on the new minimum wage of £12.21 of approximately 0.4% . However, if you look at various data sources, the cost of labour to a UK business as a percentage varies between 15% -40% , very much dependant on the type of organisation . This would equate (even at 40% ) to the new NIC adding less than 0.2% to a company’s costs. The sort of increases facing companies on a daily basis make this pale into insignificance. Or relative insignificance. The increase in the minimum wage alone will have a much bigger impact on company costs. But not surprisingly that is not what the headlines are, as it is difficult to argue that increasing the lowest wage is a bad thing.

Here is an example:

Morrisson Supermarkets in an article on retailgazette.co.uk said the NIC would cost them £75 million. According to their 2022/23 balance sheet their wage bill was just north of £3 Billion. The £75 mil equates to 2.5% . 1.2% increase = £36 million.Their sales turnover was £18 billion in 2023.

This is not to pick on Morrisons, as I suspect other major chains have similar cost profiles. But it is very diffcult to imagine that a 1.2% increase in their labour costs would have a major impact on their performance, especially as some of this would be obviated by marginal price increases, all off which are the same for all their competitors. Moreover, in their case they are undergoing a cost cutting exercise including reducing their debt levels by 40%.

Shoe Zone, a UK retail chain of shoe shops are planning to close stores because of both NIC and Minimum Wage increases . It does not make sense. They state that their position in the market makes them very price sensitive . Well, its the same for theother discount shoe stores. And let’s remind ourselves this is the minimum wage not the National Living Wage.

The issues facing 2025 for the UK businesses ( and much of Europe) are general rising costs , very flat consumer demand, and political uncertainties. An argument over NIC is just the tip of an iceberg and enables Business to voice it’s concerns via a soft target. Some financial journalists are already saying the budget has already impacted on prices when none of them come into effect until April 2025.

Whilst I don’t see any economic growth with this budget there could be be grwoth in inflation due to the increase in NIC & Min Wage . Not terribly helpful as this will hinder and delay future interest rate cuts which would help growth.

If I have got this wrong , I would really like to know , otherwise Seasons Greetings ! And yes the last 2 images are AI generated – What fun we have …..Or is it what fun it has with us !

I hate articles that start off with a Definition of something .

So, I will start with a really bland one, whilst defining the concept of Design does everything to make something that can be so complex , so very mundane.

a drawing or set of drawings showing how a building or product is to be made and how it will work and look

Cambridge Dictionary

It pervades nearly all aspects of our lives. It is most certainly pertinent in everything we buy, whether goods or services.

What makes good design ?

What does “good” design look like and are there any instructions on how to create it? Dieter Rams, legendary industrial designer, who’s “less but better” approach inspired a generation of products, is famed for writing the Ten Principles of Good design.– www.designmuseum.org

Good design is innovative

Good design makes a product useful

Good design is aesthetic

Good design makes a product understandable

Good design is unobtrusive

Good design is honest

Good design is long-lasting

Good design is thorough down to the last detail

Good design is environmentally-friendly

Good design is as little design as possible

In the most part, this relates as well to a Service as to a Product.

Before we go any further lest not foget the wheel. 5,500 years and still going strong. I propose that there has been no better designed product. It has impacted upon every aspect of life and will continue to do so, in some form of other, for a long time to come . Nothing comes close in terms of design.

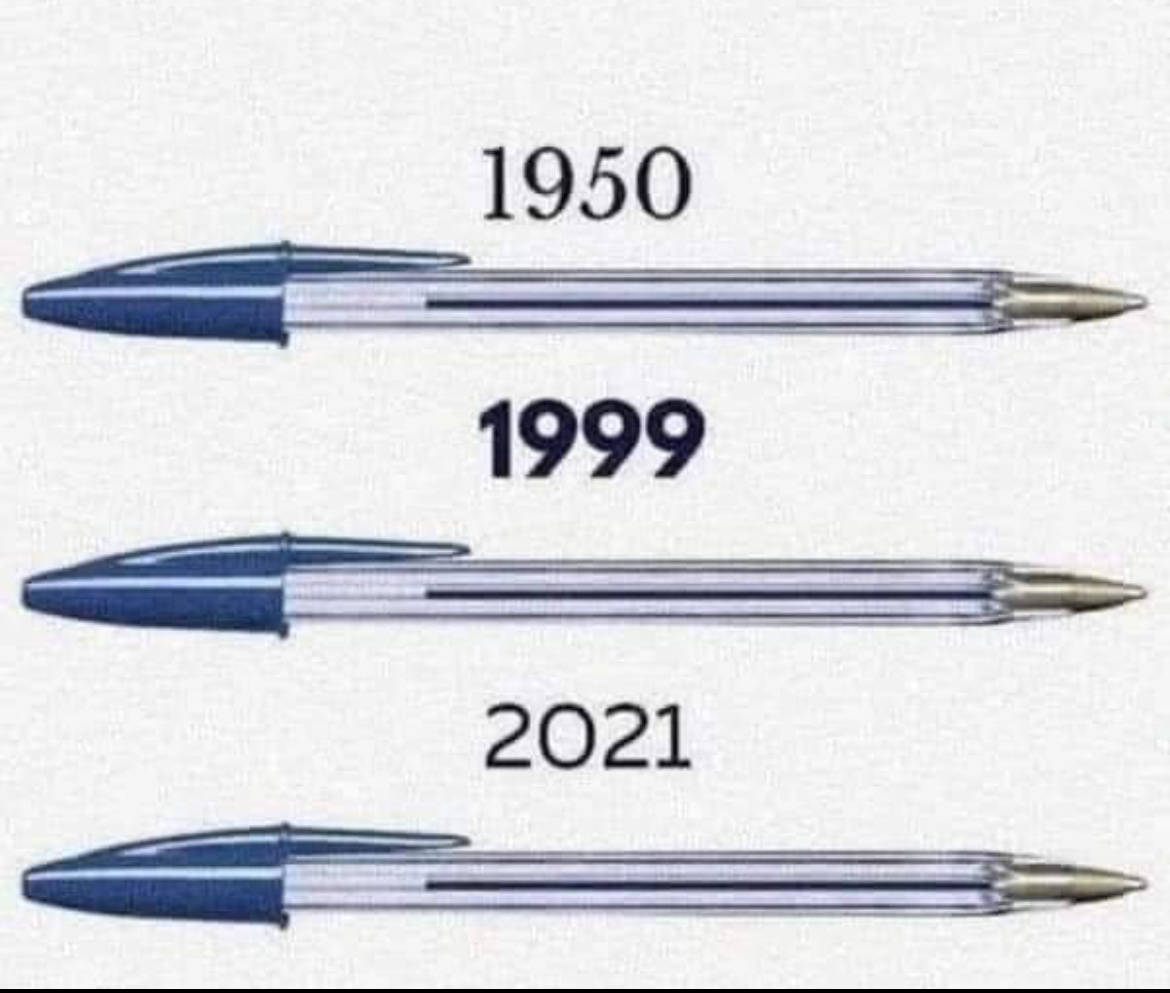

One simple product that I believe hits the mark on every count and illustrates the power of simplicity, usefulness, honest and long lasting is Laszlo Biro’s Ball point pen.

I can only think of one significant change in design and is when they put a hole in the top cap , to prevent small children (or big ones) from choking if they sucked on it and got stuck in the throat. Yes, very much a secondary use was the thinking process that was created when sucking on the top of Biro!

I stand correct on this as they have also managed to reduce the amount of plastic without impacting on design and use. See below:

I cannot come up with any equivalent low priced, effective succesful product which has been designed and as little changed over 75 years. There are many, however, corporate ‘designs’ that have stood the test of time with only subtle changes.

1891

2024

1908

2024

Clearly both of the above have changed but it has been very slow and evolutionary such as the principles of the original remain and as a generation of consumer grows that little bit older it can still connect to the brand.

Occasionally good product design can create a demand for a product that nobody really knew existed.

For me there is one stand out product of modern times. The process began with the Company name … Apple. At the time most other Computer Manufacturers had imposing names like IBM, ICL, Hitachi,NCL, NEC and Microsoft. Steve Jobs (nobody is absolutely sure why) plumbed for Apple. The machines looked different and they were the first with a graphical interface as opposed that of other systems using text. Their initial success was soon engulfed by the mass success of the licensing and creation of Microsoft and its use in most PCs worlwide whereas Apple software would work only on Apple machines,and somewhat ironically focused on the niche market of Designers. Having left and being brought back into the struggling company Steve Jobs did, what the market considered slightly bonkers, develop a product away from computers. First came the ipod, which was not only a stunning looking product but immensely practical because of its capabilities. In 2007 the first Iphone was launched to much acclaim for the way it looked but was crictised as many asked Whats the point of it?

Apple Inc created and designed The Point of it . Apple led and the rest has followed. They designed and created and product then designed and created a need for that product . Others followed . We are now at a point where in the developed market it has become a virtual essential to have a smart phone of one sort or another. Try and park your car without a smart phone . Try and book a Doctor’s appoinment with a smart phone. On a recent holiday in Italy, we went out on the first night for a meal, leaving our phones in the hotel as were on holiday, and on asking for a menu , being told to scan the QR code on the table . We didn’t do that again.

Poor Design?

Very recently Jaguar (UK manufacturer -Indian owned -Car maker) redisgned their logo. It has been treated mainly with derision . The accompanying ad has no mention of cars. Elon Musk -New Leader of the Free World – or at very least the bit of the free world that is completely bonkers – says (and I quote)

Do Jaguar make cars ?

Well, the proof of the pudding (as we say in English) will be in the eating . That said it has created an awful lot of publicity and it is very likley that someone like Elon Musk would not have even noticed the development without the controversial reviews.

You decide !

More Bad Logo Designs

The difference between Good or Bad in design , is subject to very fine margins. Ultimately, the judgement is made on how well a product or service performs. But it is not always true. Julia has a friend who often asks her what she thinks of the design of a new product she maybe launching . If Julia doesn’t like it then her friend knows it will sell . Well, some may say that Julia has no taste. To some that maybe very true, though they would be very brave to say that to her face. I would not say that. And that is not because I am worried about being smacked in the chops. It is because she has a very succesful background as a Designer .

“Design is so simple. That’s why it is so complicated.” – Paul Rand (American Desinger who specialized in logos eg IBM & UPS in the 1950’s & 60’s )

In 1996, The architects of a new Building for Salford University (Manchester UK) received the Stirling Award for Architecture (supposedly the most prestigious architectural award in the UK ). For the last 9 years it has remained empty because it is unuseable. Bad ventilation , heating system that did not work, no kitchens or social spaces …..to paraphrase

In short, it was a triumph of architectural gloss-glass, metal and concrete -over function -Richard Morrison -The Times November 29 2024

Salford Council now wants to demolish the building to build 900 homes and the Architects are furious and are objecting. They base theri argument on…

‘Ageing infrastructure is not a justification for demolition….’

It looked good but it was all form and no function .

In 1997 (clearly a bit of an iffy period in British Design) British Airways launched a newly design tail fin representing art and design from cultures world wide . The aim was to apeal to a market World wide . The, then, Prime Minister , Margaret Thatcher , when shown a model, dropped tissue paper over the tail fin. The designs were all removed in 2001 .

Several years ago a competitor of ours, launched a range of product, of which both Julia and I thought the design was really naff. We were wrong . Very Wrong. It turned out be a huge seller. Not only that, it was a product from a US company and they only sold it in the UK , making it unavailable in the US . Then they discovered that certain UK dealers were selling it on Amazon US with such a success that they made it available in North America.

Getting Design right should be a simple process. Well it is not . All the boxes maybe ticked, focus groups created, market research completed , but if launched and the customer don’t like it . The design ain’t no good . Design can be so simple, it is so important , it is very difficult ….For inspiration look at Bic and Apple . James Dyson (Dyson Vacuum cleaners) made 5,126 design changes over 4 years before his original idea worked. Even then he was rejected by many retailers. In 2023 the Turnover of Dyson was £7.1 billion . He got Design right. But nobody can tell him it was easy.

Many years ago, in a time when a Telex machine sat in the corner of the office and we all sat around it waiting for the magic to occur (once a day if you were lucky- the company may have not been busy but boy was it Hi-Tec) a colleague, good friend and much respected Salesman once said to me …

Mark, do you know who the most important person is , to me, in any of our customers ?

No, Reginald (not his real name , I would never have worked for anyone called Reginald, least of all Reggie , as he would have frightened me- for those who don’t know any 60’s London gangsters he was a nasty one. I was too young to know him but my Dad did). Do tell.

Well, it was not who you think it is . It is not the Boss, it is not their assistant , it is not the buyer …

Reginald get to the point , the telex machine might kick off.

It’s the geezer (and then it was invariably male) who takes our delivery in at the back(metaphorical back, it could be front sometimes) door .

None of this is true. Or at least the only true part is what Reginald said (and he was a very highly respected salesman) and the Telex bit . He qualified it by saying that with every customer if you did not treat everyone within the customer’s organisation with equal respect then you should not expect it in return . He used the Guy at the back door as an example of being the very first person who actually comes into contact with the product you have sold to the customer. If he can relate your inanimate cartons to a good experience then there is a very good chance they would be treated well, counted properly , stored nicely, recorded accurately and perhaps a little more patient if the delivery driver has turned up late .

It’s all about customer service . It does not stop and start with being nice to the Buyer/Boss. It’s a lot more holistic. Yet still very simple. If you are able to have relationship with all the relevant colleagues (especially with the one at Goods In) it will ultimately smooth the path from your product going in the metaphoric back door and out through the front door.

Of course the same is true in reverse . You can be the best and most liked salesperson in your market place. You maybe selling a terrific product at an amazing price but if the courier your company uses always arrives late at the customer , is very grumpy or awkward and your accounts department starts chasing payment before you have had the delivery. Or your Sales office never picks the phone up or answers emails. You will soon loose that customer. I don’t want to start on The Buyers. To be quite clear, the majority are great even if they do not become customers. That, after all, is their job , to select from whom and what they buy. And No, I don’t expect them to always return your calls. But a few are just rude or very forgetful. Missing apointments happens for a variety of reasons but not getting any acknowledgment of that is not on and I suspect that is not conducive to that company getting the best service from that supplier. Ignoring information that has been requested . Being down right rude in meetings. That happened to me in a virtual meeting when discussing possible price increase when the immediate response by the said buyer was as follows ….

If you continue in that vein ( the vein was the initial suggestion that we may need a price increase) I shall terminate this meeting now .

How is that helpful ?

We have all had the experience of going into a Retail Store, been looked after by an excellent salesperson and made a purchase. When getting home you have a query and ring Head Office, and find they are very unhelpful , don’t have an answer, or can’t be bothered find out, don’t follow up on your query and try pass it onto another colleague. Not only do you seriously consider never going into that shop, it also tarnishes the Brand of product you have bought .

It does not matter whether in a commercial or consumer environment, there should be seamless good customer service. The principles are very simple in my book. Yet many organisations consistently fail the test from all angles. That includes …..

We are sorry our phone lines are extremely busy right now ….

Lucky old you …

Treat every individual (within a specific organisation), you react with , with respect

Clarity and understanding in expectations. By that I mean understand what are the limits of that colleague , within the organisation, is able to achieve within their brief. An example would be that I would not necessarily ask the receptionist how many missing cartons there were on a specific delivery. However, if your relationship with that customer is very good the Receptionist may say I will find out for you . In the same way, as a consumer, I went back to my retail store and asked some detail about my new Smart TV, and the Salesperson said Sorry I don’t anything about that model but I will find someone who can . I would be just as disposed to that store as if that same Salesperson was doing the assisting.

Life is short, relationships come in and out of your life at high speed, and sometimes you get only one chance to make it work. Showing kindness means that when you look back at your career, you’ll be proud not just of your achievements but how you went about them. Wherever you sit within an organisation, it matters. There’s kudos in kindness.

Richard Harpin is founder and chairman of HomeServe and Growth Partner, and owner of Business Leader magazine

None of this is rocket science. Yet most days most of us will receive from one organisation or other (big or small) a transaction of some form or other that is well below par. There can be many reasons for this , some of which can be excused because of personal situations, such as, not well, had an argument before leaving for work, recent bad news ….. but most can’t.

A short post but I don’t hink there is a need to say a lot, as a very famous Meerkat keeps saying …

The Rules are Simples …..

Sorry the Meerkat only says SImples . And for overseas readers see link for Meerkat explanation ( albeit he is Russian) https://www.comparethemarket.com

Oh, well, a-bless my soul, but what’s wrong with me? I’m itchin’ like a man on a fuzzy tree My friends say I’m actin’ wild as a bug I’m in love I’m all shook up Hmm, ooh, yeah, yeah, yeah

Elvis Presley

I am fascinated by World Politics but am not even remotely qualified to comment apart from the ‘bleeding‘ obvious, it is all shook up , at least in the Western Democracies . I am fascinated by the party market, remain unqualified but have at least enough years within the market, feel I can have a vaguely qualified opinion. For those who don’t know, I am not referring to THE Party market, in terms of having an apparently great time , throwing vast quantities of alcohol down your throat , a quantity of ‘Party?’ drugs, playing monotonous music and in some cases hours and hours of sex ! Well that’s what I have been told. I mean balloons, fancy dress, and party decorations. Sex and drugs maybe involved but not within the Retail Market place. I think? That said I am a bit like the Drug dealer who says…..

Never touch ’em meself. I just sell ‘em.

Or at least those I watch on telly say that! I don’t go to parties but I sell the stuff that is used to create a party atmosphere.

When £70 million plus is spent on Glastonbury Festival tickets, in a matter of hours after the official web site opened for 2024, the Party market is struggling to find consumers who will spend any money to have a party at home . This is not a UK problem , I know for certain this is a world wide malaise.

Within the last 2 months, 3 of the leading brands have encountered severe financial issues. Smiffys, Amscan and Qualatex (Qualatex in North America problems started over 18 months ago) the three leading brands in Dress Up, Party and Balloons, are in the process of being restructured in one way or another. How and why has this all happened in such a short period and at virtually the same time ?

Traditionally the Party market has always weathered Economic downturns . I can remember quite clearly that during poor economic climates in recent decades it has stood up well and in some cases flourished. The consumer whilst strapped for cash, stopped going out or having celebrations in third party locations stayed at home and spent what they had on making the home party, the fun place .

So what is different? A maelstrom! I am averse to hyperbole but I think in terms of context , it is not hyperbolic. It is, if nothing else, a perfect storm and below I have bullet pointed in no particular order my reasoning. I will, then, qualify them in a little detail . All of these I believe are relevant in Europe but what I can gather is it also true of most consumer based societies.

-Covid

-Cost of living

-Change in consumer behaviour

-The Chinese

-Market Changes

Covid

Covid has been used as answer for a whole load of stuff. However, there is a lot of validity in many of the rational, massive change in consumer behaviour, supply disruptions, peaks and troughs in demand. Some of those peaks being slightly false because they were magnified by shortages of product . All the many implications highlighted long standing weakness in the supply chain.

Cost of Living

Without doubt has had a huge impact over the last 12 months. It may seem a little supercilious to say Why? As it is blindingly obvious. Yet it is not as simple,as above, in previous recessions party has faired well. The next 3 points have a lot to say about Why?

Change in Consumer Behaviour

Covid has had a major influence on consumer behaviour. I don’t really think anyone knows quite what those changes are. However, one very obvious change and example within the party market was the use and consumption of balloons (especially Latex) . It created a huge boom (more bubble in my view). Consumers being at home watched loads of youtube videos on stuff like Balloon Decorating and wanted to get in on the act whether for personal amusement or for starting a business. There was plenty of online information on how to do this and for a start up business it was very inexpensive to get set up. And set up they did, in their droves.

Going from the market being starved of product , the market is now over supplied and many of those who started small decorating business have discovered it was not quite as easy as they thought and it certainly was not as profitable.

This, however , is only one example, there are many others , yet for the most part, and I repeat, none of us know as to what they are .

Part of this change maybe along the lines of an article I have just read concerning Treatonomics . This, according to some journalists in the UK Times Newspaper, is where those on a reasonable income , but have little disposable income splash out on having fun. Generally involving going to some event or other. It has come to light when Barclays Bank has estimated that the recent Taylor Swift Tour in the U.K generated over £1 billion in additional(not including Swifts own take) revenue. This is just not ticket revenue, but hotel, travelling, eating out , drinks and everything else involved on going to a major concert. It has a term , yes, you are quite right, swiftonomics. It is not only confined to the UK as most other cities where she has performed are recording a similar impact. Moreover, some heads of state are asking for her to perform in their countries. Chile was very peeved as she decided on Argentina and Brazil . ‘What about the Chilean swifties?‘

The Chinese

This is not about the current concerns among Western Governments’ security concerns, or a poke at he national identity of the Chinese nation it is rather more direct and obvious.

As a market place we have just about got our heads around Amazon & eBay . Both heavily laden with Chinese Product. But it has not stopped there. We, the party market, have the likes of Themu, Shein, Aliexpress (Thanks David Beckham -see TV ads) to contend with. It would be very naïve to think that these have not sucked a load of consumer demand away from the traditional supply chain. Within that chain I would include home grown B2C webshop buying from local suppliers as well as market place sellers and Independent Party Retailers.

Market Changes

Prior to 2020 there were indications of market changes. For example within Party dress up, there was a consumer move away from full costumes to dress up accessories. Certainly in Europe, the costume market had peaked and was at a plateau. Within the general party market , which had developed enormously over the last twenty years, there was a feeling that it had a come to a standstill. I couldn’t count the number of customers who said ‘we need something new’. Of course there was and is a lot of new product but general it is always a variation upon on a theme. The consumer has or is changing and we have not been changing enough within the market supply chain . Circumstances now tell us we have to.

So why have 3 major brands all gone down at the same time? Is the market over supplied? Probably. A big problem within a relatively small market ( it is not mobile phones, cars, or fashion . We are talking about occasional purchases generally of lowish value) is that when a Brand dominates a market, it is difficult to achieve growth. As a consequence I believe some of the bigger players have made errors in their operations because they were striving for double digit growth or at very least market domination. If you supply all the major outlets in your market place where are you going next ? Just as significant is if you loose a major player or have your range reduced, how do you replace it ? I can only speak in terms of the UK but I am pretty sure it holds true in Europe, that the majors are supplied on a much reduced margins. If that were the case in many cases it would only act as contribution to overheads, losing that business means no contribution to overheads. Where do you go to replace this business when you are a Brand leader? An oversimplification perhaps, but it illustrates some of the problems facing big brands. What are the options ? Less turnover bigger margins. Old saying…..

‘Turnover for vanity, profit for sanity’.

But that, of course, is only part of the problem. There are other structural issues that are not easy to quantify and certainly not in a short blog. Whatever, the case the failing of major brands, it is not good for anyone. It is not good for employees, it is not good for the market in general as it creates uncertainty, at a time where there is already much uncertainty and it is not good for all the suppliers of these brands as they loose major customers, monies owed and most probably losses on existing deliveries much of which can not be diverted elsewhere. I know the latter to be true as having been contacted by a couple of such suppliers. Also it possibly leads to a short term influx of cut price merchandise . This may sound great to some , but is just one more destabiliser and devalues the stock already within the chain.

In the medium to long term the market will stabilise and the existing supply chain will learn from past mistakes and truly take stock of what the market needs and how it will operate . I am still very positive about the future of the Party Market going forward. I think it will come out of it much cleaner, more efficient and greater understanding of how the market will be in the coming years.

Why the Elvis song ? Well the title works , the image perhaps not, the lyrics definitely not but for those who don’t know, the owner of the new Smiffys, owns Graceland !

The exact origin of the phrase is unknown, but the first recorded use of the phrase “the elephant in the room” was in a 1814 fable by Ivan Krylov(a Russian writer of fables). In the fable, a man goes to a museum and sees an elephant, but he doesn’t notice it because he is too busy looking at all the other small objects on display.https://nosweatshakespeare.com/quotes/famous/elephant-in-the-room/

There can be very few conversations, meetings- commercial, international, diplomatic, personal, virtual or in person that have not had Ellie, in various sizes, present. It is a most unfortunate metaphor. Elephants are highly intelligent and social creatures. To use them as an illustration of difficulties and problems that were rather not discussed is somewhat disingenuous to the very regal Elephantidae family.

It is the problem that no one or group, or organisation wants to discuss. Invariably, it is the one thing that needs to be discussed. If not, at sometime , it will stand up and tell everyone ‘I am here’. When that happens the problem will be much magnified because its consequences and potential resolutions have never properly been talked about.

History is quite literally littered with examples.

In the 1950s, the phrase was used to describe the issue of racism in the United States. At the time, racism was a major problem in the country, but it was often ignored or discussed in hushed tones. The phrase “the elephant in the room” was a way of acknowledging the problem without directly addressing it.nosweatshakespeare.com

Europe has been ignoring Immigration for some years . Rather, it has lightly discussed the problem (as seen by its populations) and developed fragmented policies of varying types thinking it would go away somehow, but failed to talk about it seriously and openly . Politically the Elephant has stood up, raised its trunk and trumpeted I’m here , what are you going to about it ?’

Scientists have been aware of issues concerning Climate Change for a not inconsiderable number of years. Surprisingly so were some politicians.

1989 – UK Prime Minister Margaret Thatcher – possessor of a chemistry degree – warns in a speech to the UN that “We are seeing a vast increase in the amount of carbon dioxide reaching the atmosphere… The result is that change in future is likely to be more fundamental and more widespread than anything we have known hitherto.” She calls for a global treaty on climate change.BBC News September 2013

It took the best of the next twenty years for it talked about with any seriousness. The Elephant that I think still exists is that nobody has said if the targets that have been set were met , would it definitively make sufficient difference. Then if they were met and it made little difference, what would be the next step. Personally, I think it is not widely discussed because it would be feared that society would probably say ‘why bother?’

“There’s a phrase, “the elephant in the living room”, which purports to describe what it’s like to live with a drug addict, an alcoholic, an abuser. People outside such relationships will sometimes ask, “How could you let such a business go on for so many years? Didn’t you see the elephant in the living room?” And it’s so hard for anyone living in a more normal situation to understand the answer that comes closest to the truth; “I’m sorry, but it was there when I moved in. I didn’t know it was an elephant; I thought it was part of the furniture.” Stephen King

He goes onto say ‘ the clever ones recognise the difference ‘.

However, there are times when thinking ‘furniture’, as openly accepting that it is actually an elephant can have unintended or even unwanted consequences . Serious consideration of those very consequences need to be assessed before telling others in the ‘room’ that there is a bloody great elephant there.

When two elephants fight, it is the grass that gets hurt. — African Proverbs

There a still a lot of buts . Sometimes the Elephant may be standing behind a long curtain and you are not sure if it is a trunk hanging out the bottom of the curtain or a giant Cobra. Or just a lamp stand.

Whistleblowing, in an odd sort of way is often about elephants in the room. Although, a number of individuals can be aware of various issues but cannot/will not reveal them because they are under pressure not to and will face their own consequences unrelated to the issue. It is peer pressure in various poses that stop the elephant being discussed.

In the UK there is a legal framework to protect Whistle blowers within the work place but it is by no means fool proof.

The two main barriers whistleblowers face are a fear of reprisal as a result of making a disclosure and that no action will be taken if they do make the decision to ‘blow the whistle’UK Gov 2015

On a more micro level i.e. personal, small business/industries, this actually a very difficult subject to examine as by talking about specifics, you actually have to talk about the Elephant . Doing that exposes problems that people do not want to be made public. This post came about through an associate within our industry said why don’t you post about a certain issue that has always been an Elephant. I responded by suggesting that if I did, someone might put a contract out on me. So I wont.

So here is a really big Elephant….

BIG ELEPHANT

Image Courtesy of Me

So here is a conversation between Advanced Economies and China.

So look here Mr China (it’s Mr, as China, as is mainly run by men) we have had enough of your cheap product, made by underpaid and oppressed workers , subsidised loans, poor human rights, and suppression of minorities. We still need very cheap stuff as our cash strapped society needs many more cheap T shirts and clothing. We are going have our stuff made in Vietnam and Cambodia where the labour is cheaper (and then all of the above oppression, rights etc etc and many of the factories are still owned by Chinese). And don’t you start going on about Western Importers having made fortunes for last seventy years bringing in all this stuff. We are definitely not complicit . We needed this stuff and it helped our economies grow especially those of our High Street retailers.

Mr China replies:

Welcome my very good consumer based economy friends. We are very aware of these issues and therefore have taken some steps to help you out. We have set up companies such as Shein, Temu, Alibaba, and Aliexpress so that your hungry consumers can still buy very cheap products direct from our factories without disturbing your very busy importers and retailers. We thank your very generous governments for giving us preferential shipping rates, ignoring counterfeit product and non conforming product standards. We thank the British Royal family who having made the wonderful Mr David Beckham a sustainability ambassador for you ever so Gracious King. We have paid him handsomely to promote our Aliexpress marketplace of selling very cheap product and many times filling airplanes with this wonderful stuff. You might have seen him recently on your Giant TV screens ( which we also make- so everyone wins – well we do anyway).

The more I think about it the more I see loads of bloody Elephants. It is a bit of shame really as Physical Elephants are wonderful creatures . The metaphoric type can rarely be wonderful, it must be being cooped up in all those rooms that make them such troublesome creatures.

There, I have written about the Elephant room . that will please someone , and if they read this they will know who they are .

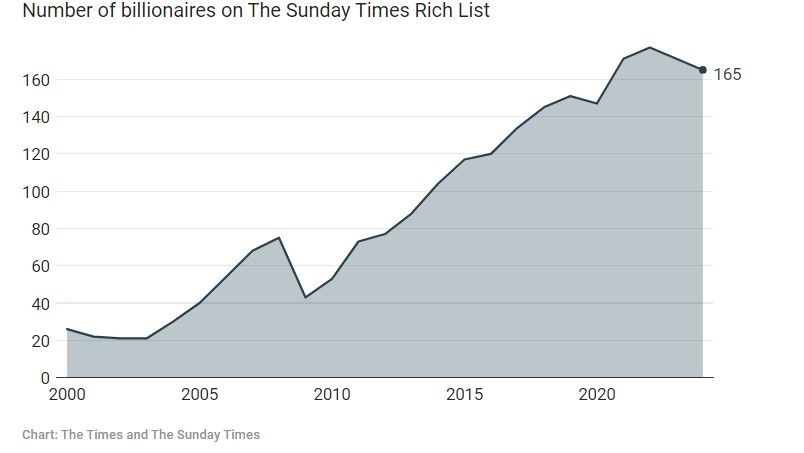

Every year the Sunday Times Newspaper issues it’s Rich List . Every year (nearly) I post about it .

It is not that fabulously rich people fascinate me. They don’t . Or rather the famous ones don’t but the ones I have never heard of, are rather more interesting. Check out https://www.forbes.com/billionaires/ This gives some background and detail of people you may never have heard of. I am also interested in where is this money and what happens with it.

According to the report , there has been a decline in the number of UK Billionaires. As the measure of wealth invariably involves stock values , the UK market was pretty flat in 2023 thereby decreasing the wealth of the few. However, the picture is not always that clear as Forbes , who measure in dollars as opposed to sterling show no such decrease.

Apparently there has also been an exit due to the changes in the Non Dom Status ,as well as their children being mugged for their watches. An oversimplification but if you walk the streets with a twenty grand watch on your wrist you are making yourself a huge target , and saying ‘look what I have got and you will never have‘. Some would say this would never happen in Dubai. Which is probably true but not a realistic or desirable comparison.

What I do not understand is why , if you have assets of £1 Billion sterling or just a mere several hundred million do you need to up sticks and move to some distant region to save even more. What is the point of this excess wealth? Much of it will never be spent. The combined wealth of the 350 in the list exceeds £795 billion. That is a massive amount of money . To what avail?

An example, an Entrepreneur called Alfie Best (not a Billionaire , mere £947 million- here’s another odd thing they don’t say how his valuation has nearly quadrupled within the last 12 months ) ,just ordered a £500,000 Rolls Royce is moving to Monaco (for those who don’t know he owns and runs numerous caravan parks, many are not especially happy campers- most are actually the homes of the owners-as he has a reputation of being quite ruthless in his management style. ) They will be either earning a very average wage, or pensioners and do not have the same opportunity of moving elsewhere.

“Britain needs to wake up — we are losing wealth creators,” he grumbles. “Our tax system and business regulations are sterilising the few strong people who build economies. We need these people to start businesses and create jobs. Brexit was a golden opportunity to create a fast-growing pro-entrepreneur environment. That chance has been completely squandered.”

So if that were the case why were the other (lets assume some might ) 325 other multi millionaires not moving elsewhere and managing to eek out an acceptable lifestyle despite paying the same percentage tax as do millions of employees within middle management.

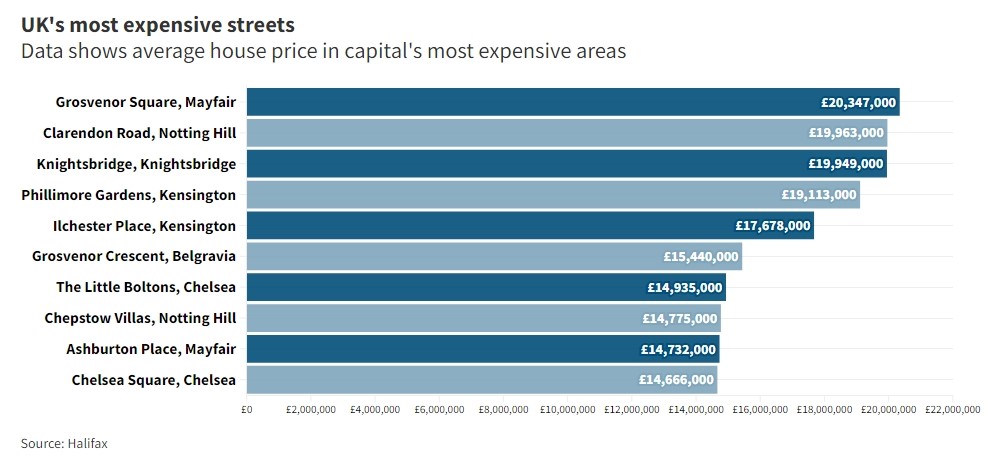

“London is really the problem. A lot of houses in places such as Belgravia and Chelsea now look very, very expensive. You won’t get back what you pay for them. It takes an age to get anywhere in such a congested capital city, especially with 20mph speed limits. If [the government] hike taxes the departures will become a stampede.” Anonymous Billionaire quoted in the Rich List.

Now I live in London, and yes the prices of properties in Belgravia and Chelsea are eye watering.

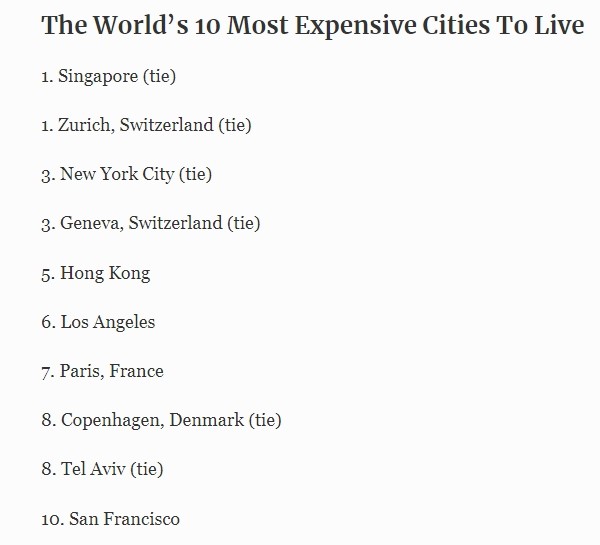

However, these are the World’s expensive cities to live according to www.forbes.com

And according to www.moneyinc.com the most expensive cities for property were Monaco, followed by Basel (Switzerland) and Palm Beach Florida. London does not feature in the top 10.

For the most part these are wealth creators, so along the way they enable many jobs, some very well paid and some not so’ but whatever the case they create money that is in some way spent in various economies. It is the vast wealth that they accumulate that can never be spent .

If you have several billion in your bank account how does that make any difference to your first billion.

Most billionaires suffer from a singular fatal trait: they simply don’t know when to call it quits. The sharkish desire for ever-increasing levels of success gobbles up everything in its wake. Reviewing the life stories of Richie Riches such as Bernard Arnault, the LVMH boss, and the Amazon founder Jeff Bezos is a lesson in how the magnetic pull of money warps normal life. Marriage becomes a contractual nightmare — look at Bezos paying out nearly £30 billion to his ex-wife, MacKenzie Scott, in their divorce —

Zing Tsjeng Saturday June 01 2024, 6.00pm, The Sunday Times

So where do the big bucks go? Property, planes, cars, yachts, divorces, jewellery , and lets not forget in some cases philanthropy. to put it in perspective Zing Tseing in her article calculated….

If someone gave you £10,000 (approx $12,500 or €11,600 )every day, you’d still need 274 years to become a billionaire.

The accumulation of vast wealth is exactly that an accumulation for, as far as I can see , just for the sake of it. It brings power and plus a whole load of baggage.

Elon Musk is apparently the wealthiest man in the world . His wealth equates or exceeds (by an enormous margin) to that of the GDP of over 140 of the World’s nations . Or put another way he could feed cloth, house every body in Zambia for each year , for 10 years and still have enough for his planes, trains(don’t know if he has any but makes the comment slightly amusing?) and automobiles .

I am not condemning extreme wealth, wealth creation, or the accumulation of wealth. But I am questioning it. If you stuck your first £1billion in the bank it would earn you £50 million p.a. That is nearly £137,00 per day. Why do you need more ?

I am also aware that as the valuations use stock values the super rich can loose the super bit very quickly. Phillip Green is a great example of no longer being a Billionaire , much in part due to the value of his stock. This is also true of many Chinese Billionaires whose wealth is tied up in property and the collapse of the Chinese Property market. The Forbes list of Billionaires runs to 2600+. That number in terms of world population is not huge but the combined wealth is $14 trillion. That is greater than the combined GDPs of India, Japan, Germany & the U.K . 2600 people have more wealth than 4 of the world’s largest economies put together, leaving only the USA and China has having larger GDPs.

So that might be were the big bucks are , but where do they go ….?

Ever since the human species started selling stuff, there has always been a New Kid. Today we would call them disruptors.

A bloke on a horse (they would, invariably, have been male) would have replaced the bloke on foot walking from camp to camp flogging stuff to the camp dwellers. For horse insert donkey, cow, camel, goat or whatever was the local form of four legged transport

Carts were added to help carry more stuff

When the camps got bigger no doubt the local entrepreneurs would have built some sort of semi permanent stall

Eventually permanent buildings ( A shop) would have been erected

The next step ( I think) would have been a group of shops, selling the same stuff , owned by the same entrepreneurs having them located in different towns. Thinking about it this could have been the first disruptor in the retail market place. A shop liked by the consumer because they did not have to travel to other towns to buy these products and bought them at better prices because the entrepreneur paid less for them as they bought in bulk . The very same reasons other retailers would have hated them. Thereby disrupting the market as opposed to purely developing the market

Department stores

Mail order

Chains of Department stores

Supermarkets (disruptor)

Huge supermarkets (disruptor)

Discount stores (not sure about this one)

Convenience stores

Online shopping

The market places eg eBay & Amazon etc (big disruptors) but very different animals

Social media platforms ie Facebook, Instagram & Tik Tok, combined with the use of Influencers(disruptors)

For sometime now, Mr Bezos and his garage start up has been the scourge of many a retailer worldwide. At the same time it has also created many multi million dollar sellers .

Getida

Is there any other retail operator that make this claim? Apart from some of the world food franchises eg McDonalds and KFC et al, I doubt it . What is more, the majority of Amazon’s profits are made from its cloud computing operations. Such as hosting a big chunk of the U.K. government’s operations including that of HMRC . Yes that’s what you’re thinking, all my tax returns? It amazes that me that many still don’t realise this including a number of accountants I know. Yes, next time you post your Vat returns you will see them fly off to AWS cloud .

But this is not about Amazon, there is a new kid on the block . I believe this one is much more insidious.

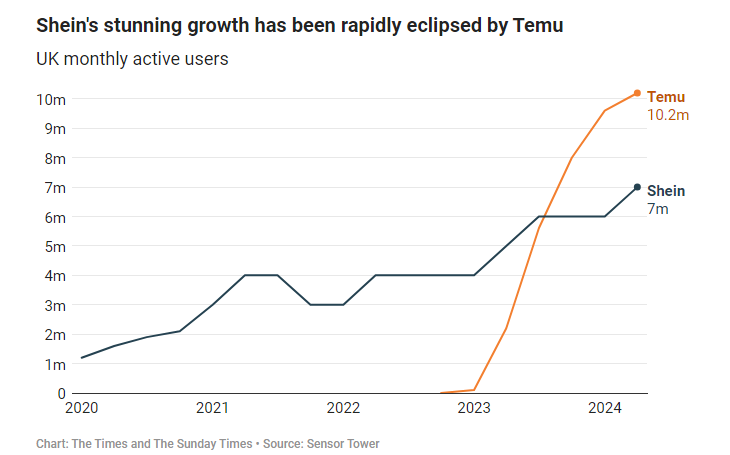

I posted about this particular beast in 2023, detailing its extraordinary growth. Temu is it’s name, disruption is it’s game.

Below is a chart, which represents its parent company Pinduoduo, rapid growth in the US.

It isn’t that by buying from Temu , you can seemingly refurbish a four bedroom house for £13.50. It isn’t what may actually turn up in your door step a few weeks later may not be quite exactly as the image you bought from. Neither is it that the quality of said goods might mean you have to refurbish your house again a month later . Nor is that the likelihood that any of these products meet any quality or safety standards. I see none of this as a problem as I feel the consumer worldwide is more canny than that. They will get over the novelty and quite literally use it as a giant novelty gift shop .

Most of us would think it would only be the Gen Z generation who were hooked by it . The stats below ( once again from the US) show the complete opposite.

This alternative Perfidious Albion goes much deeper. Before I go any further , I have waited a long time to use that phrase and I am not completely sure , I have got it right this time but look it up and hopefully you can see if I have.

1. They are amassing a huge amount of data

2. They are scraping the ocean floor of keywords relating to their product areas creating havoc on many online stores specialising in those products .

Amassing a load of data is no new thing. Amazon have been doing it for nearly thirty years. Temu have been doing it less than thirty months. We, sort of, let Amazon do it as they provide products the Consumer likes and wants and if the product is not right Amazon sorts it. Their focus has always been on the consumer . Consequently the consumer is very confident buying from Amazon. As far as the Temu’s of this world are concerned they just provide very cheap product and I don’t see that as a long term business model .So what is their plan….

I am none the wiser.

The keywords issue is having a big impact on online web shops. Within my own industry , I have stories where they have hijacked over 40% of the relevant key words. This has had an immediate impact on their business. If I type in google Party shops in Leicester (or any other town in the UK ) Temu will come up first or second. This, in itself, is not usual . But this has happened very quickly and is very disruptive.

There have been other disruptors in recent years such as Alibaba & Shein. Shein employs approximately fifteen people in the UK as of last September. They have also opened various pop up shops and acquired some brands such as Misguided. Yes they are very cheap but from subjective sources the quality is poor. In the US there is an 88% awareness of the brand but only just over 20% satisfaction rate (Statista.com) . But it is very clear as to what their mojo is. Cheap, throw away fashion. I am not sure we know what Temu’s is ?

In a slight aside Shein is looking for a listing either in New York or London, with a current valuation of approximately $60 Billion (down from $100 billion). Some financial journalists believe they are looking for a listing as soon as possible , whilst the valuation remains relatively high as they are being constantly being scrutinised for manipulation of EU & UK tax laws concerned with import duties, in addition to age old agreements on very favourable local shipping rates.

If a company fills a container with items, they can say they are all individual consignments and escape the duty — but in reality, it’s a container load of goods. It’s an abuse of the system,” Richard Allen, a campaigner with Retailers Against VAT Abuse Schemes (RAVAS).

Yet some observers wonder whether this also betrays a fear that stiff competition from its rival Temu, which has quickly aped aspects of Shein’s tax-lite model — as well as the prospect of regulatory crackdowns on fast fashion — will mean Shein’s stratospheric rise could soon level off. Sunday Times May 5th 2024

The tax laws referred to, refer to Temu as well . Low value single items (£135 in the UK) are treated as gifts with import duty .In many cases these single items are bundled together in a container still avoiding import duties but benefiting from lower courier rates and the benefiting from much lower local postal services.

This is a bit of an oversimplification but it illustrates of the nature of the beast we are all dealing with.

How we deal with it ? I don’t know. The French have decided to have a go

Brands that churn out cheap clothes and constantly change their styles face penalties of up to 50 per cent of the retail price in a move to offset their environmental impact.

Advertising is to be banned for fast fashion retailers, whose clothes are usually binned within months and end up in landfill. Unlike traditional brands which renew their collections four times a year, politicians claim that fast fashion brands offer thousands of new products every few days, causing pollution and encouraging their customers to keep spending. Sunday Times May 5th 2024.

As to how they can decide what are Cheap Clothes and how many new products are too many remains to be seen. However, going back to the start of the blog, there have always been disruptors and they will continue to appear and disrupt.

i suspect many thought about six years ago Jeff Bezos would be untouchable , or at least the retail version. Then came along 2 disruptors capturing billions of dollars of consumer spend from nowhere . Very soon there will be another. The extra ordinary thing is we don’t have any idea what format that new kid will take and who they will disrupt.

My Customers will start ask me the perennial question…How do you think the new year will be. I am very succinct and precise. It could be good or bad. That’s it in a nutshell.

There is a footnote to this response that is not always obvious as depending who the customer is I do not include this is in my ‘six word ‘ financial forecasts.

I am very clear in my own head ( as if anyone is any doubt ??)

I am not a financial analyst

I am not a retail analyst

I am not a market analyst

I am not an analyst

But I am frequently asked the question at the beginning of the year by customers, colleagues, Julia , A few friends ( very few that confined, in that I only have a few , very few. To extend my audience I have asked Aristotle ( our dog) and his canine response is I am only interested in three things …

Walking (currently it is -5 degrees but that doesn’t bother him )

Food

A massage

As long as my face and the sound of my voice assures him, that is the only interest he has in the coming year.

There is undoubtedly a number of gloomy indicators out there , especially for the first three months. Cost of energy, continuing Ukraine crisis, inflation, interest rates , consumer confidence, industrial unrest, and a lot of uncertainty within the World .

So what’s good about 2023

Inflation appears to be peaking and below what was forecasted

Interest rates whilst still rising are predicted to be well below original forecasts

Sterling has recovered some of its losses

Covid does not present the same barrier it has for the last 2 years

Fixed mortgage rates have reduced a little

The survey of 138 companies, including 50 retailers, found that a net balance of 11 per cent of businesses said sales grew, up from -19 per cent in November (CBI)

A Coronation (at least for the Party Sector in the U.K. )

Retail landlords are starting to become a little more realistic

This does not detract from it being potentially being very tough, but it should be put into some of perspective. The total retail sales within the U.K. in 2021 were £421 billion . There were approximately 316,000 retail outlets. If retail sales fall by 3% that equals £12 billion . However, if we look it another way a consumer who had £100 in their pocket to spend freely may only have £97. If you extrapolate that further and look at the total U.K. spend on party (of which it is really difficult to find a true figure) even if was half of 1% of total retail spend which would be a gross over estimate , we are looking at targeting less than 50p of the consumer spend .

There will be many (gross exaggeration) readers who will say don’t be bloody stupid ….that’s only £30 million total party market. It is quite clearly many times that but the principal is the same . Within our market place our target audience is a very small proportion of their overall disposable income.

Twixt the optimist and pessimist The difference is droll: The optimist sees the doughnut But the pessimist sees the hole.

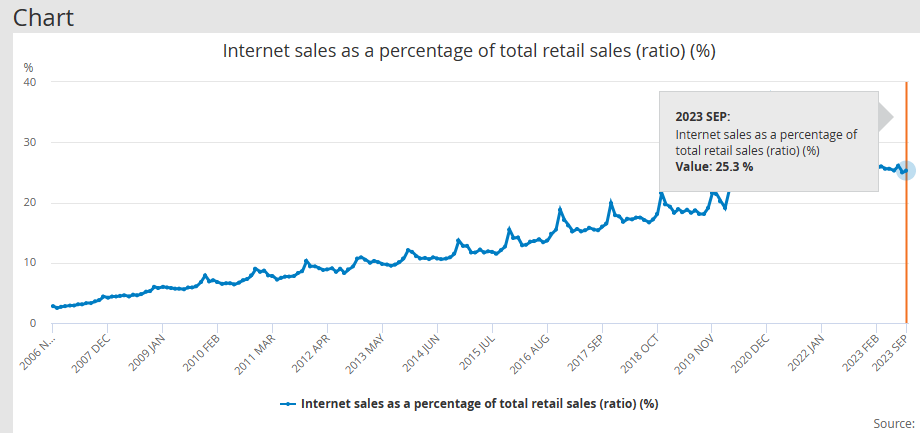

For every £100 we spend , £75 is spent in a shop ( or it’s brick equivalent).

I last posted about this about 6 years ago. Little has changed apart from the share of online has naturally increased, but the drop in market share post Covid is evidence that purchasing online is not always consumer heaven.

More importantly is that not all about consumer preferences . It is also about the complexities of selling online.

Or rather not in the way displayed by the guy above.

I am, in terms of probably having been an exhibitor at about 140 trade exhibitions during my working life time. Over 80% of those I have been involved in the building and taking down of said exhibition stands. Moreover for the last twenty years plus I have been a Director of Exhibition Company. If that makes me an exhibitionist in the same way as someone who does art is an artist , then so be it.

I return to this subject on occasion, as it is sort of the end of the season for my market place in terms of significant trade shows (party, Christmas, toys and cards) so the issues , and they are mainly issues, are fresh in my head. For purposes of my own clarity of thought, something quite difficult for me to achieve, I shall split this into three sections, Organiser, Exhibitor and Visitor (Buyer).

ORGANISER

Like anything, there are good and bad. As a generalisation they fall into two camps: Big & Small. The Big ones in my experience are the worst offenders . By ‘offenders’ I mean rubbish organisers.

My personal experience of large organisations running trade shows is down to one Exhibition and many different companies running it over at least forty five years(at The NEC, in total it has been running for over 70 years) . The Show concerned is the The Spring fair held every year at the NEC in Birmingham in the UK . It became one of the largest English Speaking Consumer Goods B2B exhibition in the world . The breadth of product ran from Furniture, Fashion, Jewellery , through to Luggage, Household and even Party . It filled all 20 Halls (190,000 sqm or 2,000,000 sqft) . There were over 3000 exhibitors and upwards of 70,000 visitors from all over the world . It has an extraordinary location , in that it is in walking distance of Birmingham Airport , Mainline train station (direct from Birmingham Central & London Euston) and quite literally minutes away from an extensive Motorway network , which can take you all the way the Glasgow, London, Manchester & Newcastle without a traffic light. A great deal has changed since 1976 when it first opened and most Exhibitions (Worldwide) have suffered falling numbers, both in terms of exhibitors and potential buyers . Yet the decline with this show has been even more dramatic, now not being able to fill 8 Halls and around only 1200 exhibitors.

How So ?

Like many large operators an element of arrogance. When the show was full and there were waiting lists there was a great deal of ‘you will do what we want you to do even if that is not best for your company ‘ attitude. During later years as the decline (partly due to the changing profile of the retail market place )this persisted but in a different way even under different owners . This manifested itself in many ways such as constantly re-organising Halls , re-organising stand locations ,even when being promised a stand location if booked early only to be moved . This happened three times to a friend of mine in 2023 .

Then there was the year that they proposed parking charges, suggesting somehow this was good thing. There was uproar and they capitulated . In 2023 they ( with a fanfare ) were going to add a substantial (additional I may add) marketing fee to each exhibitor for the use of contact software which buyers would use to make 15 minute slot appointments on stands. Once again claiming this was an amazing opportunity (obligatory) for every exhibitor . Following, what was probably an exhibition first at least in the UK, Industrial Action(better name for gentle riot) at the Autumn Fair . Another 180 degree decision making process. And finally (trust me there are lots more) in an email to prospective visitors they trumpeted wonderful new benefits eg Extra seating in the Halls (or rather aka lack of exhibition stands ) and a happy hour drinks late afternoon for buyers . Well thanks very much exhibition organiser for a super way of sucking the potential buyer away from visiting stands. That said if it did happen I don’t know of any buyer that made use of it.

For Good Organisers trying looking at smaller shows (Christmas & Gift in Harrogate for example ) . Of course I am biased .

Exhibitors

Organisers sell space and market the show to potential buyers. Exhibitors rent the space dress it, display their product and focus on getting their target buyer to come to the show and visit the stand . Simples, as a well known Meerkat says. For the most part exhibitors do this well. Well at least creating a welcoming and effective area of display. What some do , and it is a minority but a largish minority, they rely on the Organiser to bring in the punter. They have a responsibility but if you are a exhibitor, who has spent a lot of time and money on your space, it is you that should target your potential customer base and get the visitors to come and to come to your stand. If a major buyer attends the show and does not come to your stand it is not the fault of the Organiser. The blame lies elsewhere.

If a group of buyers that you would expect to see are at the show but don’t come to you. It is not the fault of the Organiser. The blame lies elsewhere.

If those buyers pass your stand and don’t come on . It is not the fault of the Organiser. The blame lies elsewhere.

Lastly, if they do come and never buy from you it is not the fault of the Organiser. The blame lies elsewhere.

The exhibitor has to work hard to find out who they want to come , then if they are coming inducing them to visit your stand and when they do make it an interesting and informative experience.

Seeing it from both sides of the counter , I find it quite extraordinary that companies both big and small who have spent not an inconsiderable sum on showing at a trade exhibition and then display (sometimes very poorly- display that is ) a very laissez faire attitude towards the very organisation’s they presumably want to trade with or at very least open a channel of communication. Then to make it even worse fail to follow up after the show.

Buyers(Visitors)

There are Good and Bad. Without argument there are considerably less in number -no matter the market – than there were twenty years . Take my own industry, there were over 350 wholesalers ( of various shapes and sizes) of Greeting cards about twenty five years ago, maybe thirty. If only half of those visited any one relevant trade show there would be three to four colleagues, from most of the visiting companies, equalling over 500 visitors. Today there are barley a dozen (and that is generous figure ) still trading today. If two colleagues from half of the companies came to a show today , it equals 10 visitors. Moreover that 10 would each spend less time at the show as against the 500+.

Unfortunately the Good & Bad have a similar impact on those depleting numbers.

Bad

Looking at Bad, is actually quite complex. As Bad can mean various things.

Buyers who just never go to a trade show. If you don’t you quite literally do not know what you are missing . It maybe nothing but you don’t know unless you go

Buyers who go but don’t look . Rather they do look but only at their existing suppliers

Buyers that suffer from that horrendous affliction of Trade show over enthusiasm. I have seen the symptoms so many times . They visit your stand . Are very enthusiastic and tell you to contact them afterwards. When doing so ( contacting them that is ) never take take or return your calls. Even worse they take your call and haven’t a ‘scooby do ‘ as to what you are talking about . The worst scenario which has only happened to me a couple of times. They actually do take your call. They make an appointment . Then when you do turn up, they don’t or ask why are you here ?

Those that that don’t tell you who they are . I appreciate that some of the bigger buyers don’t want to be hassled but I’m sure they are professional enough to be able handle unwanted advances . If you, the seller, don’t know who you are talking to, you can’t best inform or help them.

Good

Those that spend good quality time at relevant trade shows , talking to existing suppliers about future developments in addition to looking for those who may have products and services that they would not have come across and would add value to their business.

Those that understand that exhibitions are not just about buying stuff or looking for stuff to buy. They are also about networking. Talking to suppliers and maybe competitors. Very often it is the only time especially with smaller operators that they get to see wider pictures of what is going on in their market places . It can go further . Looking at trends not necessarily directly related to your own product or service category but those areas that indirectly affect your business.

How about that ? It’s much easier being a Good buyer than a Bad buyer.

Over the last fifteen years or so the role of the Trade Exhibition has changed enormously . The three parties (organisers, exhibitors and visitors) that do not recognise this, will be party to the continuing decline of trade shows. They are no longer places for taking or placing orders. They are no longer events that will attract visitors in the numbers of days long gone.

If the Organiser does not provide a facility that is affordable and welcoming, the exhibitor will no longer exhibit. The Organiser will fail . However if the exhibitor and visitor still wants a relevant event, an alternative Organiser will appear. If they decide they don’t need a show then a show won’t happen .

So in conclusion Organisers need to raise their game

organizatores certaminis, cave

Trade show organisers, be aware

A bad exhibitor’s business won’t necessarily fail because they have a rubbish stand . It won’t help but it won’t fail.

A Buyer’s business won’t necessarily fail because they don’t go to an exhibition. It won’t help but it won’t fail.

Eventually an Organiser’s business will fail if it is a rubbish Organiser.