I make no apologies apart from to the authors . I have plagiarised the majority of the data in this post from a report Schematic IQ –Johnson Controls (via Retail Gazette) . I would have no personal access to this kind of stuff.

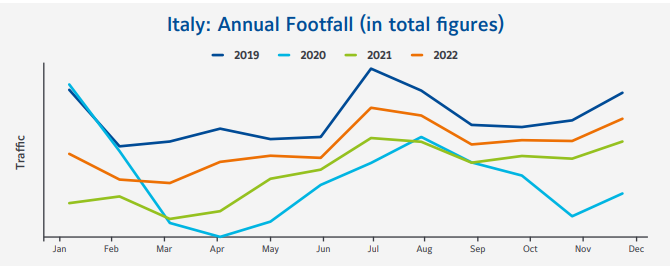

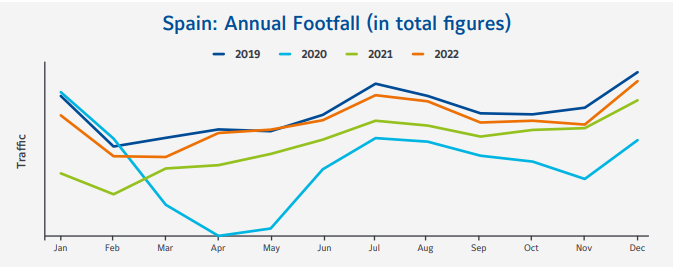

Much of the stats that are below are from 2022 . Not altogether surprising as it is only March 2023 . However I think as what happens in one year tends to influence the following year , they are remain useful . I have also looked at some European comparisons in order to illustrate that the patterns are very similar .

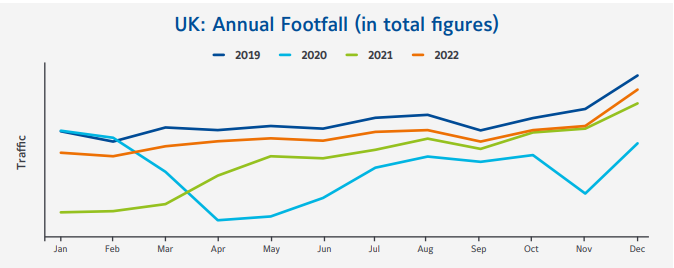

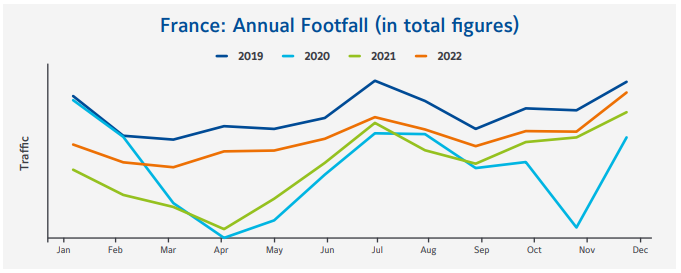

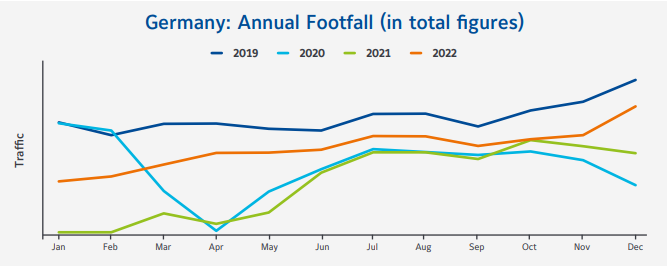

Another significant year to look at 2019 ( which all these illustrations include) . It would be very easy to use this as Benchmark of where we should all be vis a vis Pre and Post Covid. What this does not take into account of are other major psychological events that have also occurred. The war in Ukraine and political turmoil in the UK, to name but two.

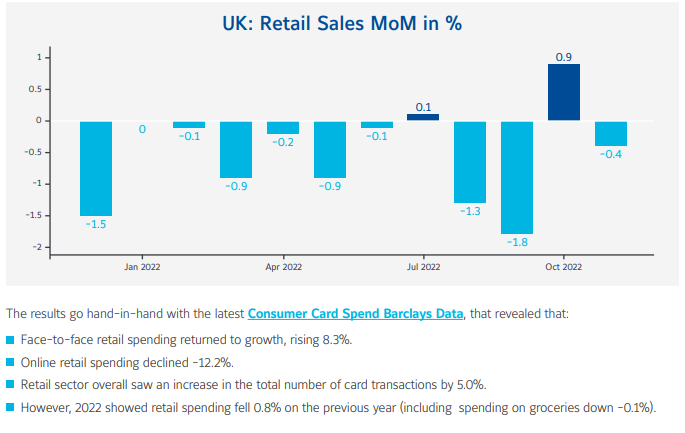

Whilst none of this will be much of a surprise as in the early part of the year we were still under some form of Covid restrictions, plus the Ukraine War starting, and the latter part of the year , in the UK we had a huge amount of uncertainty courtesy of the Tory Party, and finally huge Energy prices increases. Great year for a boost in Consumer Confidence ! That all being considered the stats don’t look that bad . Other significant changes were the decrease in online spending and the increase in Bricks & Mortar.

Using the illustrations I thought this would be helpful for Retailers , from wherever in Europe. Most experiencing similar troughs, and peaks throughout the same period. For those who do not think Sport plays a major part in our economies should look at the French Chart . At least in part, the sharp rise in Nov/Dec was attributed to them reaching the World Cup finals.

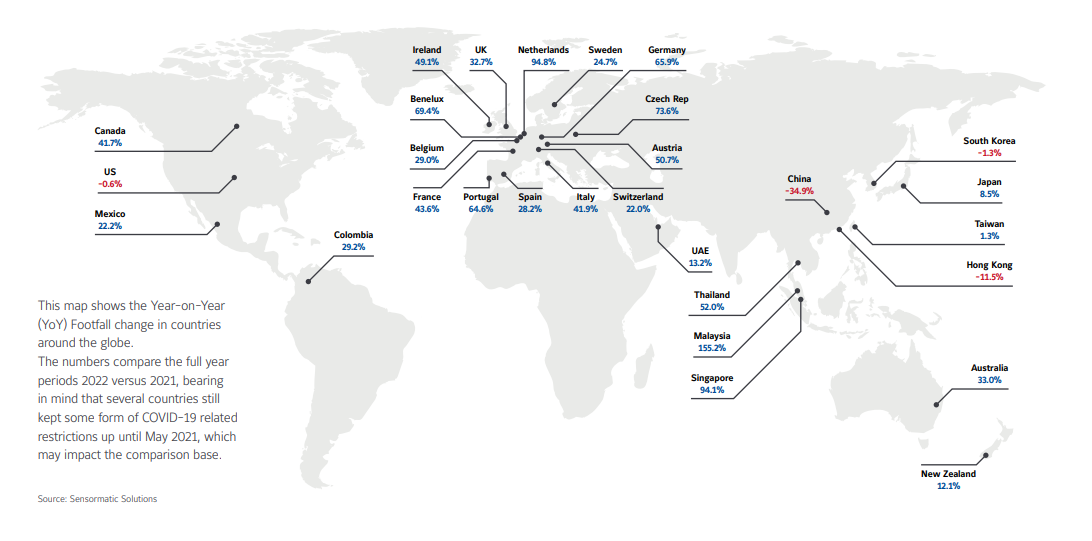

And finally the World view. Naturally those numbers in blue are the increases and in red the decreases .

Whilst footfall is really important, it does not always relate to what goes through the till. Nor does it say anything about ‘now’ . Of course , it couldn’t as it was conducted last year . A number of my customers have been surprised that January and February were not nearly as bad as they expected . Some of this will be explained by inflation. Prices have gone up, hence whilst their takings are holding steady, they are actually selling less product. There are minor benefits to this. If you are increasing prices along with their inflationary cost increases you are still make the same gross margin but actually taking as much cash through the till but having to do less work for it. In theory.

It is a very mixed picture. Some major retailers are facing very difficult times e.g. John Lewis et al . But I am not sure this about the health of the High street as opposed to the health of any particular chain and the changing retail landscape. It is certainly not all about the threat of online although many retailer’s would argue otherwise. Online share of the UK retail market has actually dropped within the last 12 months.

The chains are more about looking at structure and data analytics (guess what, so are online operators). The independents are more about ( or rather they should be) service levels, variety and range of stock and developing their profile with their local community.

The one thing we can learn from Covid is that the Independent can be very resilient and innovative . If they were able to survive the very unhealthy High Street of Covid then they will undoubtedly thrive in a retail High Street that is somewhat less sickly than it was in the previous three years. The Multiples have different issues to contend with that go beyond the general demeanour of the Consumer. I just wish some of the big organisations would stop using Covid as an excuse for poor service levels . Weekly I get an email from my bank HSBC starting with….

Due to the impacts of the Covid 19 pandemic its become increasingly difficult for our call centres and processing teams to maintain normal service levels.

HSBC Reported profit after tax increased by $2.0bn to $16.7bn year 2022

Come on Bank ,your profits are very healthy , put a bit towards making your service levels healthier or at very least up date your standard emails .

Sorry, I digress. But even HSBC is still on some High Streets .

Despite all that is going here and abroad there are still many healthy retailers and there will continue to be so. The key to health in whatever form is if you’ve got it, the tough (read ill for the human) times are easier to handle and more likely to lead to a positive outcome.

Retail sales as measured by volume rose by 1.2 per cent in February compared with January, according to figures out this morning from the Office for National Statistics. The increase, the largest since last October, exceeded City expectations for a 0.2 per cent rise.

Strong discount department stores drove a 2.4 per cent rise in non-food sales. Food sales, by comparison, were up 0.9 per cent.

Aled Patchett, head of retail and consumer goods at Lloyds Bank, said: “A rise in sales for February suggests that consumer confidence is heading in the right direction after a difficult few months.”

The Times 24/03/2023

I believe there is a direct corelation between our own health and that of any retail business..

Humans

- Eat well

- exercise mind

- exercise body

- sleep well

Retail

- Eat well – Making sure you have good quality stock . Dont just look for deals . Ask why is a deal being offered . Look at them as fast food -quick & easy but not conducive to healthy retailing . Continually look for new product

- Exercise the mind -Be creative and proactive

- Exercise the body- Interact with your consumer , look at ways of improving customer service. Do what the multiples cant

- Sleep well – when the business is shut for the day make sure you do as well

To keep the body in good health is a duty… otherwise we shall not be able to keep our mind strong and clear.

Buddha

All this plagiarising was done by my human AI (Artificially Intelligent)and not an AI Bot 😂