What is it ?

It’s doing stuff !

Or rather, spending money on doing stuff.

It is not a new term, as it has been around since the early 2000s. The term was first used by 2 economists back in 1998, but the theory goes back a lot further to Alvin Toffler’s book The Future Shock, published in 1970. But it is the last twenty years, when it has become a very significant part of Consumer discretionary spending.

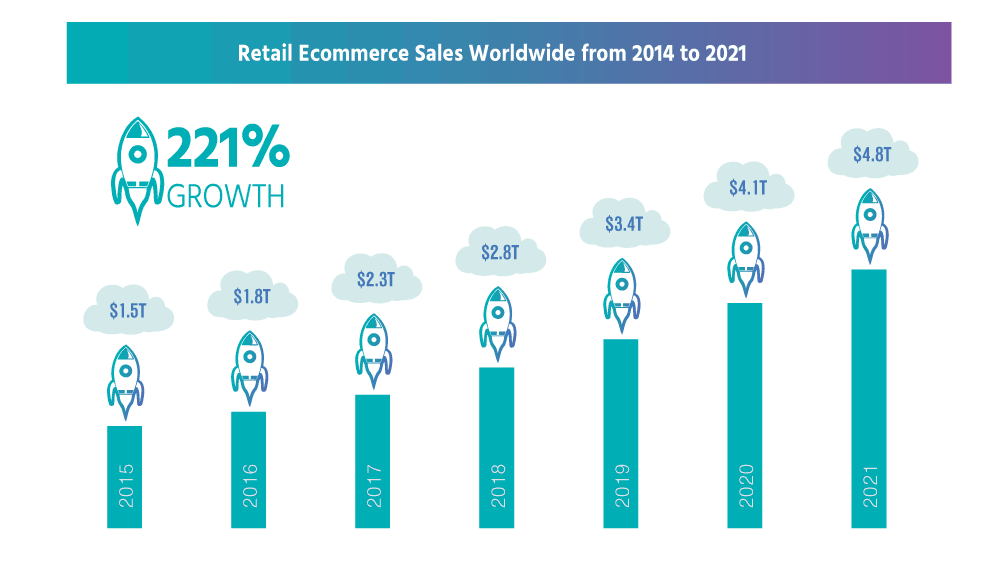

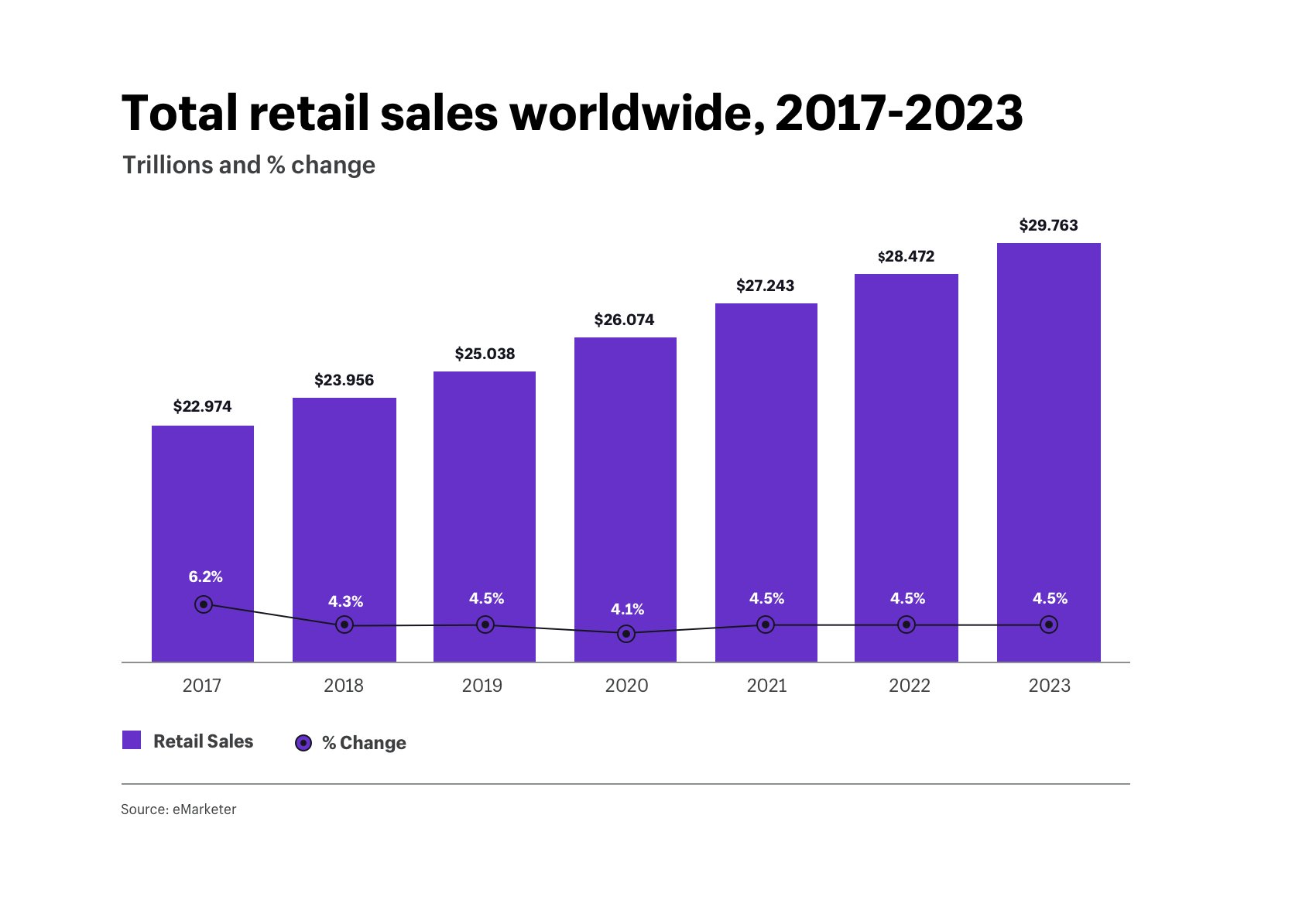

For investors continually looking out for the next big trend, it’s hard to ignore the sustained staying power of the consumer experience economy (both digital and in real-life) – expected to reach $2.1 trillion by 2032.

Nasdaq March 2024

So what sort of things are we looking at :

Indoor Crazy Golf

Indoor Archery

Darts

Indoor Amusement Arcades

There are few large towns in Europe that do not have at least one Escape Room experience.

These are just the tip of the iceberg, as the total economy includes Concerts, holidays, events, and a bucket load of other occasions where a single or group of consumers spend more on experiencing something as opposed to just buying a product, for the primary reward of enjoyment. This has an exponential impact on consumer spending within the wider economy.

Six in 10 (57 per cent) say they would rather spend money on a good experience than on buying material possessions, up 5 percentage points compared to corresponding Barclays research from 2018, and nearly two thirds (63 per cent) would rather tell people about something they have experienced rather than something they have bought. Similarly, four in 10 (44 per cent) are actively seeking out new and unique experiences to make the most of the summer – a figure that rises to 61 per cent for 18 to 34-year-olds.-Barclays Research 2024.

The figures are enormous. It is estimated that the Glastonbury Festival contributes over £160 million to the UK economy. Eating out, new outfits and Taylor-Swift-themed afterparties were also set to contribute to an overall boost of £997m to the UK economy (BBC March 2024). There is nothing new about festivals or concerts, but what are relatively new are, as above, the immersive experiences

The obvious losers in this are those in Hospitality. But I think that is sort of missing the point. Every retail outlet that looks for the discretionary spend can lose out, and in many cases, probably are. Hospitality is part of the Experience Spend, or certainly should be. Yet Pubs,and restaurants in the UK are all facing tough times. It is no longer just about throwing pints down your neck or eating as much as you possibly can in the ‘all you can eat’ buffets.

If your business is not an obvious player in this market, how do you access this spend? With difficulty. Within my own marketplace of Party, it is really important that you keep well informed of any of these events that maybe occurring within your locality, as there will be opportunities to attract participants spend particularly where there is any level of dress-up involved (See below where both Glastonbury and Music concerts attract a level of dressup)

There is, often, a more deep-seated problem with independent businesses both in hospitality and retail. Many tend to be reactive and not proactive. Locally to me, there are many restaurants, a large number struggling with the lack of spend. About seven months ago, there was a new player in town. A great deal of money had been spent on refurbishing an existing operation that was not doing especially well. That was just the beginning. From Day One, it has been a roaring success.

Why so? The offering is first class, insofar as the service is top notch (much of the team is very young and inexperienced – it is about leadership and training), the food and drink are excellent, and there is a terrific atmosphere. But it does not stop there. They are constantly engaging with their client base. There are the obvious occasions, such as Mother’s Day & Father’s Day, Easter, but they pounce on every possibility. Only recently, it was apparently National Fish & Chip week. Virually every week, they give a reason (and small incentives) to visit their operation. Most of the competition will be offering great food, good service, and possibly fair prices but they are not engaging.

There is a distinct vibe amongst many; It is very tough out there. There is a cost of living crisis. The consumer is not spending. Of course, there is a lot of truth in those few words, apart from two words in particular: Not spending. They are spending, but they don’t have so much to spend . Or that can be filtered a little further, there is a chunk of the population who have less to spend and they are spending it elsewhere.

None of this is unique to the UK economy; it is reflected in most European States. There are plenty of universal challenges to Retailers of any sort. Very recently, a report in the UK illustrated that food sales were down in May. It was suggested that some of this may be due to the new weight loss drugs and the consumer dramatically altering (or being altered) their eating and drinking habits. Clearly, this will not only impact food stores but a whole chunk of hospitality. Those offering ‘all you can eat buffets‘ will have to be especially creative. ‘All you can eat salad ‘ doesn’t have quite the same ring .

Whenever you are looking at your takings and consider that the problem is entirely that the Consumer has nothing less to spend, just think of this weekend (last weekend June 2025).

UK -Glastonbury -210,000 people have paid £373 per ticket (£78 million +)(cheapest ticket, there are VIP packages) plus their ex’s.

Beyonce’s recent 6 performances at the grounds of Tottenham Hotspur Stadium attracted 275,000 grossing £45 million.

There is some spare cash around; you just have to find ways for your business to have its share.